Are women at a disadvantage for reasons too numerous to list? Is it sexism? Are females not good savers? Big spenders? Is it really true that women get paid less for the same work performed? Is the world financially stacked up against women?

I read lots of articles noting all the reasons that “women have it harder” than men when it comes to saving for retirement. Regularly listed are the following:

- The difference in men’s and women’s wages, also affecting their Social Security amounts later – but the articles don’t give honest insight into why the wages vary. This leads the reader to conclude that it’s sexism that determines pay.

- Women often live longer than their spouses “forcing” them to live on one SS check instead of two – However, by women living longer, this gives more time for their investments to compound.>

- Women take off work to raise children or to become a caregiver to a family member, thus affecting their career path earnings. See the tools offered below which – if used – both stay-at-home-moms and caregivers can become financially independent.

Think Outside the Box

I don’t enjoy reading articles that tell me “statistically,” I’ll be settling for less and that I don’t have options. Or, that “according to the numbers” – somehow – I am doomed to a mediocre savings rate and career path. Or, because I am a woman, I’m going to have it tougher in life – all across the board.

So, let’s think outside the box for a moment.

First Things Frst – Education and Career Choice

It’s called OPEH.

OPEH is an anacronym for Occupation, Position, Education and How many hours worked a week. These four things affect a person’s income far more than one’s gender.

And we, as women, have choices in all of these categories.

Occupation:

Georgetown University composed a list of the best paying college majors and the percent of men and women majoring in those fields.

The highest paying majors were Engineering, Math and Science. Men dominated these job choices, so their career path was set to earn a good, solid wage with upward mobility.

The lowest paying majors were those in Psychology, education, and social services. Women dominated these fields, so their career path was set to earn less than the above-mentioned choices that males made. These different career choices limited their upward mobility within their jobs.

We women have a choice as to what field we want to excel in, and we need to choose wisely.

Position:

Teaching young girls the value of STEM courses (Science, Technology, Engineering and Math) will place them in careers where they will earn more. Upward mobility in STEM careers is greater and this will translate to better earnings on their future bottom line.

Education:

Within those STEM fields, males tended to gravitate towards a specialty or training that paid better. In other words, males once again made different choices for their focus. Nothing is stopping us from making these same choices. Our brains are every bit as good, wouldn’t you agree?

Hours Worked per Week:

Even within the same job categories – and this is important here – one of the things that differentiated male workers from female workers was the willingness of male workers to put in more hours per week on the job. Males were more inclined to be on call or be at the office any time the firm might call them.

Two other things separated the male workers from female workers – 1) men were willing to take on hazardous jobs and 2) they were willing to relocate in order to advance their careers.

If an employer wants someone on call, working many hours a week, and willing to relocate for their own advancement, we women can choose otherwise, but there is a financial consequence to that choice.

The effects of OPEH need to be explained to female children early in life. If they want to place themselves on an even playing field in their careers they can do so. At least they would know the options they face, and in this way, they can make more objective decisions about their futures.

But Wait! There’s More!

Ok, ok, so your daughter is more artistic, or leans toward community involvement and verbal skills. Is she pre-destined to never become financially independent?

This is where you as a mother, father, aunt, grandparent or friend can teach these young girls about how to invest early in their lives. And the earlier the better.

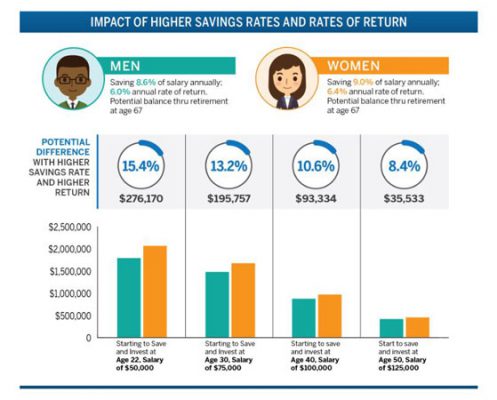

The earlier you start saving, the better your returns – Chart by Fidelity.com

They need to learn how to save and why, and to take advantage of any employer-sponsored savings plans. Teach them about the power of compounding interest, and to become familiar with the language of finance. This will pay off exponentially. If they learn to track their spending from a young age and they know where their money is going, they will become the master of their financial future.

Money doesn’t care what gender you are or what color you are, it works the same way for everyone.

Once you learn how to create a money machine and how to keep yourself out of debt, you have some powerful bases covered.

Additionally, help this child list her skills. Have her know what she is able to contribute to any company or relationship and teach her how to construct friendships and alliances so she can build personal capital. Often, it’s who you know that can give you a leg up in the world. Teach self-sufficiency, and independence.

Help her become the director of her life, not a victim. In this way, perhaps she will become an entrepreneur. Owning your own business is a well-known path to creating wealth.

These Tools Are the Great Equalizer (no matter what career she chooses) and will be able to move your child forward toward a financially stable future. Women who have chosen to be stay-at-home-moms can still be financially independent if they utilize these above-mentioned tools.

Yes, it is being done. Today.

One Last Thing

I say this all the time, and while it’s not a popular idea, it needs to be placed into the mix of valuable instruments that a young woman can use to her advantage.

Of the four categories of highest spending in any household, the cost of housing is the highest. Have her use this knowledge to her advantage.

New research shows that those who are saving significant amounts for their financially independent future, slash their housing costs. It’s the number one thing they do that separates them from the herd.

The biggest house is not always the best use of capital.

You can cut out your lattes every day and pack your lunch to work, but that will only reap you a small yearly amount. Paring down an expensive mortgage (which can be a liability) can save you thousands during this same time period. In this way, she can move quickly to her financial goals.

Additional Resources and tools

Calculators, Worksheets

– Tools and calculators to analyze your monetary situation in all areas of living.

Financial Education

– Forums, newsletters, sites to learn about investing, articles about money, market quotes

The Effect of Parents/GrandParents on Teaching Children About Finance

Parents remain THE top source of financial advice for most women. Even after graduating from college, a low percentage of women say they feel equipped to manage their finances. Today, 88 percent of women say more financial education would provide them with greater confidence in directing their money.

Help your child build a foundation for financial independence. Help her to invest as early as possible, and compounding will do the rest. Even if she takes off time to have a family, her money will continue to work for her.

After all, isn’t financial self-sufficiency what it’s all about?

Did you enjoy this article? Become a Kuel Life Member today to support our ad-free Community. Sign-up for our Sunday newsletter and get your expert content delivered straight to your inbox.

[gap height=”60px”]

About the Author:

Billy and Akaisha Kaderli are recognized retirement experts and internationally published authors on topics of finance, medical tourism and world travel. With the wealth of information they share on their award winning website RetireEarlyLifestyle.com, they have been helping people achieve their own retirement dreams since 1991. They wrote the popular books, The Adventurer’s Guide to Early Retirement and Your Retirement Dream IS Possible available on their website bookstore or on Amazon.com.

{kind=link}