Guest Blogger: Akaisha Kaderli

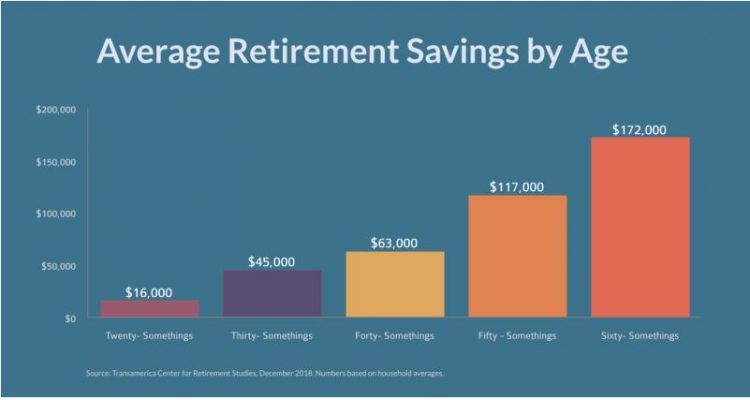

Annie is 65 years old and has as little as $200K Savings

Chart of average retirement savings by age

I know many of our readers are not “average.” However, if “Average” Annie can support her retirement on as little as $200,000 savings, imagine what you can do with the amount you have!

By reading the chart below, you can see that the average spending for retirement households age 65 – 74 is $46,000.

Chart, Average annual household spending by age group

It is tough to make that $46k amount with only Annie’s savings, so what should she do?

Social Security

The average recipient today collects $1,461 a month, or $17,532 a year. Annie’s SS check is average and she has a husband who also collects the average Social Security amount.

$17,532 times 2(people) = $35,000 per year.

Not quite the $46,000 that they need but getting closer.

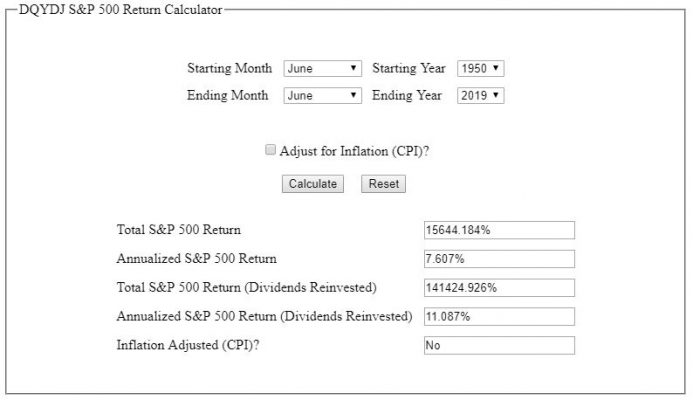

Hopefully Annie has her retirement money invested in VTI (Vanguard Total Stock Market) or SPY (S&P 500 Index) and is making market gains equaling around 10% annually.

DQYDJ S&P Return Calculator 1950 to 2019

Here you can see that since the 1950’s – about when Annie was born – the S&P 500 has had an annualized return of over 11%, dividends reinvested, but let’s use 10% as a more conservative projection.

Remember, Annie has to make up $11,000 to match her average spending ($46,000). But let’s give Annie an extra one thousand dollars per year so that she can pamper Mr. Annie with occasional gifts and dinners out.

So, she needs $12,000 out of the $200,000 in savings per year to make up the difference in spending. That’s an extra $1000 per month.

Invested in the S&P 500 – based on 69 years of returns and using 10% as the annual return – after her first year she would have $220,000 minus $12,000 withdrawal = $208,000.

Now Annie has $47,000 in annual income: $35,000 from Social Security and $12,000 from investments.

Plus, her $200,000 has grown to $208,000, a 4% gain outpacing inflation at the current rate of less than 2% per year.

Their Social Security payment is also indexed to inflation so as inflation rises, so will their Social Security.

If Annie and her partner live to be 90 years old, after twenty-five years of this illustration (see above left chart), her savings will have grown to $986,776 and perhaps she could treat Mr. Annie to a European cruise.

But what if the markets turn south and Judy’s investment starts declining? Certainly, she cannot continue to pull out a $1000 per month to maintain her lifestyle.

Adaptability is the key and – as in life – investing has no guarantees. She might consider withdrawing less and reduce her spending or she and Mr. Annie could pick up a side gig or any number of other options.

Being flexible in retirement is certainly a net positive. On the other hand, what if the markets over this timespan outperform the norms? Her spending could increase and they could go on that cruise sooner.

No one can predict the future. It’s to our advantage to develop confidence in our ability to adapt to what life throws our way.

Run your own numbers. You just might find you are closer to Financial Freedom than you think.

Did you enjoy this article? Become a Kuel Life Member today to support our ad-free Community. Sign-up for our Sunday newsletter and get your expert content delivered straight to your inbox.

Having retired at the age of 38 in 1991, Billy and Akaisha Kaderli are recognized retirement experts and internationally published authors on topics of finance, world travel and medical tourism.

Having retired at the age of 38 in 1991, Billy and Akaisha Kaderli are recognized retirement experts and internationally published authors on topics of finance, world travel and medical tourism.

{kind=link}